February 16, 2026

In September 2025, American Industries convened business leaders, policymakers, and international investors in Chicago for a high-level seminar focused on one critical question: How will North […]

Manufacturers are taking a hard look at making changes to future-proof their businesses. Yet, with so many unknown variables surrounding the economic downturn and the trajectory of the COVID-19 pandemic, most manufacturers seem to be merely forging plans, not executing on them. While manufacturers have had to reassess supply chains in the past to build in resiliency, this global pandemic presents unprecedented challenges and uncertainty.

US manufacturers could cut operating costs by an average of 23% by moving production from China to Mexico and by 24% if shifting to another Asian low cost country (LCC).

Dual sourcing scenarios (e.g., China + Mexico or Another Asia LCC + Mexico) could yield savings of 5-20% vs. sourcing and/or producing only in China.

80% of manufactured imports from China could capture cost efficiencies if produced in other Asian LCCs.

A PwC survey found 47% of CFOs across industries agreed developing additional, alternate sourcing options was a pressing issue during the COVID-19 pandemic.

A PwC comparative analysis (of US, Mexico, China and other Asian LCCs) suggests other more attractive supply-chain options for fulfillment outside of China are now on the table. This is based on numerous factors, including landed cost, risk and fulfillment lead times. Our study estimates that US manufacturers who choose to shift production from China could cut operating costs, on average, by an additional 23% if they near-shored to Mexico, and by 24% if they shifted to another Asian low cost country (LCC). We believe these and other alternatives could – on top of these cost savings – also add resiliency and improve customer experience.

Other viable and competitive LCCs, particularly in southeast Asia, have significantly improved their supplier bases and manufacturing labor forces, making them a more attractive option than just three years ago. And, particularly for North American manufacturers, Mexico is increasingly poised as an attractive option to China, especially for US market sales, given the new USMCA going into effect on July 1, 2020.

The COVID-19 pandemic is casting in stark relief vulnerabilities of global footprints that have been developing for several years. For US manufacturers of all stripes and sizes, lowering costs has been the principal motivation for offshoring. For many, that has meant entrenched single-sourcing from China, due to its historical advantages for cost and scale.

A 2020 PwC survey found that, 16% of US companies operating in China were already planning to adjust production and/or supply either domestically within China and partially outside of China – or completely out of China.[1] Of course, companies that rebalance to other regions will likely do so gradually, given the CapEx requirements and the development of other key requirements including a mature supplier network, logistics, and workforce upskilling.

[1] AmCham China and PwC China survey conducted during March 6-13, 2020

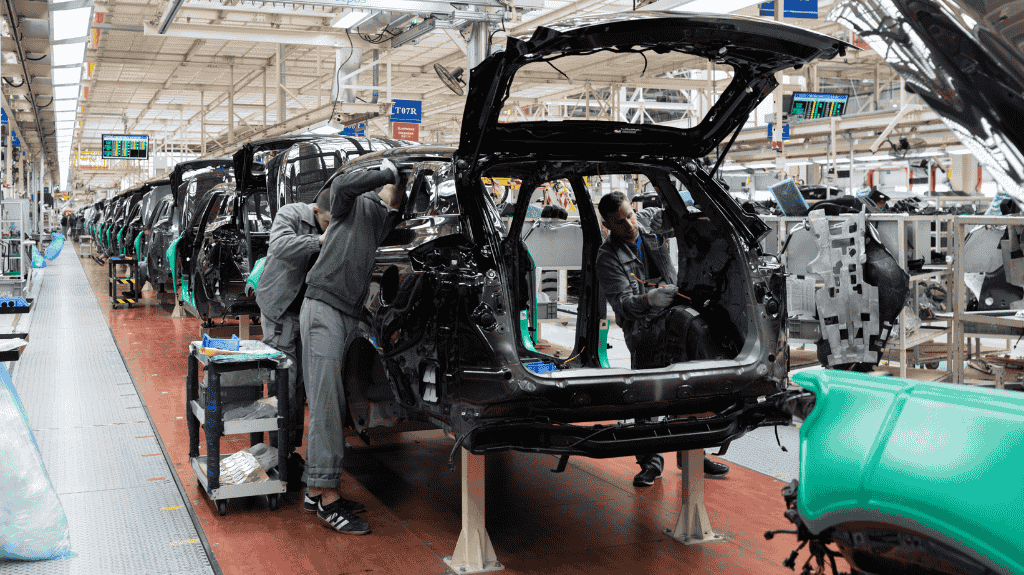

An attractive option - manufacturing in mexico

Source: PwC

https://pwc.com

Please note that we do not accept job applications here. If you are interested in applying for a position, please visit the following link: https://www.americanindustriesgroup.com/jobs/